Morten Springborg, a specialist of Global Thematics for World Wide Asset Management has written an interesting White Paper on Global Demographics and the key effects for future investing of the changing world.

Author: apcadmin

The Royal Commission – What they didn’t look at but should have!

by Robert Sarafov – Director of APC

In our recent Annual Client Briefing at the NGV, we mentioned in our presentation that the Royal Commission highlighted many examples of reprehensible behaviour on the part of the banks and AMP. However their review of Industry Super funds had much to be desired and focused on somewhat trivial issues such as HostPlus’ use of the Australian Tennis Open to reward staff.

A far more concerning issue relates to the arbitrary definition applied by some super fund asset managers of defensive assets in their portfolios, which allows the inaccurate description of a ‘high growth’ portfolio as a ‘balanced fund’.

This inaccurate description, which is perpetuated by ratings agencies and the media, then provides a level of legitimacy to the portfolio performance which investors accept as gospel.

It is a situation which is being allowed to continue by ASIC, APRA and the ACCC and is completely unacceptable and should have been reviewed by The Royal Commission, but wasn’t.

Why?

The information contained in this article has been drawn from an article written by Chris Brycki in July of this year.

Defensive assets

ASIC defines defensive assets as cash or government bonds. Cash is defensive because when the market falls it holds its value. High grade bonds can do one better and rise when share markets fall. History backs this up too; in each of the 6 times Australian shares had a down year in the past 20, bonds rose to cushion the impact. If this is ASIC’s definition, which APC would fully support and agree with, why is it that this definition is not mandated to be adhered to by super fund asset managers?

Can other assets be defensive?

This very much depends on the opinion of the fund manager and there is strong history to demonstrate why their opinions might not end up as fact.

High income stream and low growth assets

Just because an asset delivers a big income stream does not make it inherently defensive. Take Telstra. Most of Telstra’s returns come from regular fully franked dividend income but its share price has dropped 60% since 2015.

Creative definitions of defensive assets

In recent times many super funds have invented their own definition of a defensive asset which has helped to push them up the ratings. Let’s look at how some funds do this in practice. The following Industry Super default ‘balanced fund’ claims a 24% allocation to defensive assets.

The fund’s website explains that in addition to cash and fixed income “some asset classes, such as infrastructure, property and alternatives may have growth and defensive characteristics”.

Their self-defined defensive assets include infrastructure, credit, property and alternatives. These make up 22% of the 24% portfolio allocation to ‘defensive assets’. Government bonds make up just 2% and there is zero cash!

This enables the fund manager to publish a return that is included in the ‘Balanced’ table of returns however the portfolio is in fact 98% growth! As you could imagine, when compared to true Balanced Funds, it’s performance looks very good…however this is a fabrication.

Many of the top funds counted some other assets as defensive to make the Balanced fund table.

The Productivity Commission asked many super funds about returns for individual assets. Only 5 of 208 funds were prepared to disclose them!

Unfortunately and some would say amazingly, super funds aren’t required to disclose how they classify their investments on their website or to anyone. Not to members, nor the Australian Prudential Regulatory Authority (APRA) or ASIC! They also aren’t required to share how each asset has performed or even what it is. This allows fund managers to play the ratings game without anyone holding them to account.

By all means fund managers should be free to invest in illiquid unlisted infrastructure, alternatives and property assets. There are very real diversification benefits in doing so. Just don’t call them defensive assets!

Compare this behaviour to APC’s transparent approach where we publish each individual asset within the Defensive and Growth components of our portfolios AND their individual performance. This information is provided to our clients every six months in your Regular Planning Meetings.

How fund managers sell the ‘success’ of their balanced default fund

An Industry Super fund chief executive when asked about their ‘balanced’ fund’s performance cited active management!

“Over the past three years our balanced option did 10.16 per cent, while the index balanced option did 7.29 per cent, so that’s almost a three percentage point differential.

The [active] balanced option has outperformed across every time horizon” he says. It’s absurd to compare an accurate indexed balanced fund option which has an allocation of 25% to cash and bonds to a pseudo default balanced option with an allocation of just 2%.

How ratings agencies support the misleading self-reporting

The ratings agencies don’t properly query the allocations reported by the funds. This provides no check as to the real risk of the self-reported defensive assets.

Valuation of unlisted assets

Many infrastructure and property assets are held in unlisted vehicles which raises 3 concerns:

- The value of the investment is quite often based on the opinion of the fund manager and there is no way of knowing whether that value is credible given that there is no open market for the asset. This happened a lot in the aftermath of the GFC

- The financial structure may see a return of capital reported as an income distribution.

- The investment is very illiquid and a sale is often extremely constrained by agreements with co-investors, including first right of refusal and so-called ‘tag-and-drag’ conditions. One critical characteristic of a defensive asset is to be able to sell it in a deep and open market.

During the Financial Crisis some super funds stopped members from transferring money out because they were unable to sell illiquid unlisted assets. This can be done for good reasons such as protecting investor capital by not allowing ‘fire sale’ prices and therefore large losses if a manager is a forced seller in a falling market.

One industry super fund lost $1.6 billion due to poor hedging of unlisted assets. It lost its spot as one of the best performing funds in 2008 to become the second worst according to Super Ratings.

Conclusion

The fact that the Royal Commission did not even attempt to review this situation at all is quite frankly unbelievable. It represents a manifest misunderstanding of risk, as it applies to member investments. For this reason alone it should have been reviewed and the issue addressed.

However, further to this most important point, there are questions to be answered in relation to the cosy relationships between ratings agencies and the funds that they rate. The inherent conflict of interest that exists here due to the fact that the funds themselves pay the ratings agencies for their services is a structural fault of the system and does not lead to reviews of funds without ‘fear nor favour’.

We should not forget that it was the inaccurate ‘head in the sand’ approach of ratings agencies’ reviews of Collateral Debt Obligations (CDOs) that lead to the GFC. You would think that given this recent history, the Royal Commission would have allocated appropriate time to understanding and addressing this issue.

The Royal Commission has performed an important community service in highlighting shoddy practices in the financial services industry. However it has passed up the opportunity to shine a light on this particular systemic conflict of interest in the financial services sector, which is a real shame.

The lack of accuracy of portfolio information and how Growth assets are defined as Defensive impacts on the level of risk taken by unsuspecting super fund members.

This issue is gaining some traction in the media, so stay tuned.

APC Annual Client Function Presentation

In June we held our annual client function at the NGV with a private viewing of the Winter Masterpiece exhibition which was Van Gogh. In case you were unable to attend this years session we have provided the presentation delivered by Rob and Hayden on the night covering APC, the economic outlook and the performance of the Classic portfolio series. Please see the video below;

https://youtu.be/LOpbXebNUlo

Commission Rebate program milestone – $500,000 returned

As a client of APC, you will know APC is a conflict free advice firm. This means we do not accept commissions from third party product and service providers and where we do, we return these commissions to our clients 100%.

Recently we passed a significant milestone of returning more than $500,000 of cumulative commissions to our clients!

In practical terms this means our clients pay 20% – 30% less for their insurance premiums and over many years this represents thousands of dollars in savings. It can also mean the return of thousands of dollars in commission if we help a client implement a new debt facility. You may recently have seen in the media the consumer representative, ‘Choice’ advocating for the removal of commission payments from Mortgage Brokers.

Clients of APC have been enjoying these benefits for years. However they have crucially benefited from the knowledge that the motivation of our advice is not a third party commission payment but rather has simply been the belief that our recommendation is the most efficient way to achieve a desired strategic outcome that is ultimately in the best interests of our clients.

There are few advice firms that operate in this way. APC has and continues to grow mainly from our clients referring family and friends. If you know someone who you believe can benefit from our conflict free advice and personal service, we would greatly appreciate the opportunity to speak with them.

APC Team Update

Carol Tawfik

Recently, Australian Private Capital expanded our team with Carol Tawfik joining us as a Senior Financial Adviser. Carol holds a Bachelor of Business and is also a CFP (Certified Financial Planner) having some 15 years experience in providing highly personalised advice to her clients. Carol is a warm and engaging professional whom our clients will enjoy working with and will value her insights and assistance.

Carol is married to Robert, an IT entrepreneur and they have a beautiful little daughter, Alexa.

APC warmly welcomes Carol to our team.

h

Simon Ereaut and Luke Price

It is with great pride we acknowledge that our Practice Manager, Simon Ereaut and our Para Planning Team Leader, Luke Price have successfully attained the qualification of Certified Financial Planner or CFP.

The CFP qualification is the highest educational qualification attainable for a Financial Adviser in Australia and is recognised around the world in Financial Planning. Undertaking the study program while working full time takes significant dedication and is a testament to their work ethic.

Australian Private Capital is arguably in the unique position where most of our team (5 out of the current 8 team members) are CFPs. A significant achievement for our small advisory firm indeed and something we are very proud of!

h

Calypso Waddell

We also acknowledge one of our Para Planners Calypso Waddell, has recently successfully completed her Diploma of Financial Planning. Joining Hiro Matsumura, Calypso’s achievement means that our Para Planning team are all qualified Financial Advisers who continue to ably assist your formal advice team of Robert, Hayden and Carol.

Our clients should take great comfort in the knowledge that their interests are being considered and represented by a dedicated, highly qualified team of professionals. APC’s culture fosters collaboration and the sharing of ideas, which aspires to deliver the best strategies and solutions for our clients.

Dean’s Leaders Forum

As you know APC is the principal partner for the Melbourne Business School’s Dean’s Leaders Forum for 2017.

The Melbourne Business School Dean’s Leaders Forum explores what makes great leaders and encourages those aspiring to lead people and organisations to change perspectives on what leadership is and can be.

It was our pleasure to attend the school recently to hear Kylie Watson-Wheeler, Managing Director of The Walt Disney Company speak.

Pictured from left to right: Stormtrooper, Kylie Watson-Wheeler, Jim Frederickson, Kirsten Galliott, Alex Christou, Robert Sarafov and Stormtrooper.

If you would like to watch Kylie’s talk, please follow this link. It is a very entertaining and enlightening talk about one of the most iconic brands in the world. I am sure you will enjoy it and find it of great interest.

Two Valuable Lessons for Young Investors

I was recently asked to put some thoughts together for investing newsletter Cuffelinks on what advice I would give my 20 year-old self.

Thinking about this reminded me that becoming a better investor is an iterative process that occurs over many years. The only way we can improve as investors is if we learn new things as we go, likely making valuable (and potentially costly) mistakes along the way which help us accumulate greater knowledge and form better financial habits.

Unfortunately there are no do-overs when it comes to investing, and so it is with that in mind that I think about two pieces of enduring investment advice I would give my younger self.

Don’t overrate your abilities

The first thing that comes to mind when I think about my 20 year-old self is overconfidence – specifically overconfidence in my ability to beat the market. My early personal investments were concentrated in a handful of stocks, which all ended up being poor performers relative to the broad market. One of those, a US airline, even went bankrupt soon after, which was a big wake-up call.

After twenty years’ experience in investment management, I would tell my younger self how challenging it is, even for professional investors, to consistently beat the market. I certainly became a better investor once I grasped the awesome power of diversification.

Contribute early and often to make the most of compounding

Compounding really is the most powerful savings tool at our disposal. When I log into my Vanguard 401(k) portal in the US, I can see that over 20 years of saving, about half of my savings balance is from investment returns. The other half is made up of my contributions over the years.

While I have been able to contribute more over the last 10 years than the decade before that, it is those early dollars I was able to save in my 20s that have had the most impact on returns through compounding over time.

Although retirement seemed a long way off back then – and it still does today – I would be in a far better position today if I had made fewer silly purchases and put just a little extra down when I was younger.

I also would have told my 20 year-old self not to buy that Honda Prelude. This compact sports car was uncomfortable to drive on my long commute to work and the mileage wasn’t great. I should have bought the Civic, which was significantly cheaper and more practical, and then tipped the money I would have saved into my Vanguard retirement account.

Originally posted on 16th May 2017 at https://www.vanguardinvestments.com.au authored by By Rodney Comegys, Vanguard Head of Investments, Asia-Pacific

Can you beat the Market?

The Active vs Passive Debate

Australian Private Capital, over many years has observed that ‘Passive’ investment management tends to deliver a better long term return than ‘Active’ investment management. But why?……

Daniel Kahneman, Professor of Psychology at Princeton and winner of the 2002 Nobel Prize in economics probably said it best. “The idea that any single individual without extra information or extra market power can beat the market is highly unlikely. Yet the market is full of people who think they can do it and full of other people who believe them. This is one of the great mysteries of finance. Why do people believe they can do the impossible and why do others believe them?”

How about Warren?

Another interesting perspective comes from Warren Buffett who has made the point many times that high turnover, expensive managed funds (such as hedge funds) would under-perform relative to low cost, simple passive index funds over a long-time period. Warren Buffett has taunted hedge fund managers, saying that a simple low cost index fund (e.g. the S&P500 ETF) would perform better over the long run (10 yrs) than more expensive hedge funds. In fact he challenged anyone to take a bet with him that this would be the case. Buffett expected a parade of fund managers to come forward and take the bet… and “defend their occupation”. What followed was “the sound of silence”. One manager finally came forward and made a $500,000 bet with Buffett. Ted Seiders of Protégé Partners, selected a basket of 5 hedge funds to compete against Buffett’s choice, the Vanguard S&P500 ETF over a 10-year period. The bet began on 1 January 2008 and is now into its 9th year. And the results have been very interesting as the table below outlines:

The returns from the simple passive index fund have significantly outperformed the hedge funds. A $1million dollar investment in the basket of hedge funds would be worth around $1.22mill now, while an investment in the Vanguard S&P500 fund would be worth around $1.85m.

The SPIVA Report

Annually the SPIVA report is published comparing Active and Passive investment strategy performance. A high level summary to 31st December 2016 comparing Active manager’s performance against their chosen benchmark after fees over 1, 3, 5 and 10 years respectively illustrates Professor Kahneman’s point.

- 86%, 94%, 93% and 89% of Global Equity managers underperformed

- 76%, 67%, 70% and 74% of Australian General equity managers underperformed

- 82%, 62%, 48% and 33% of Australian Small/Mid cap managers underperformed

- 63%, 90%, 77%, and 88% of Australian bond managers underperformed

- 77%, 93%, 83%, and 77% of A-REIT managers underperformed

The full report can be downloaded here.

Can you know which sector will shine, before the dawn?

It is difficult to see how one could know which sectors will do best relative to others sectors when you look at the following table. Each sector has its own colour (the second table) and the performance from best to worst is arranged top to bottom (the first table). To suggest there is a pattern is a real stretch!

So, can you beat the market?

Evidence over long periods of time suggest the answer is yes, by taking a semi-passive investment approach and keeping investment costs low. By semi-passive, what APC means is structuring your portfolio to tilt to the sectors which we know, from evidence, do better than the overall market.

Academic research has identified these sectors of securities that have delivered higher returns (or premiums) over time. These premiums may be positive or negative in any given year. Over longer periods, historically the expectation of positive premiums increases. Structuring your portfolio to target these sectors helps increase the reliability of outcomes.

So what are these sectors?

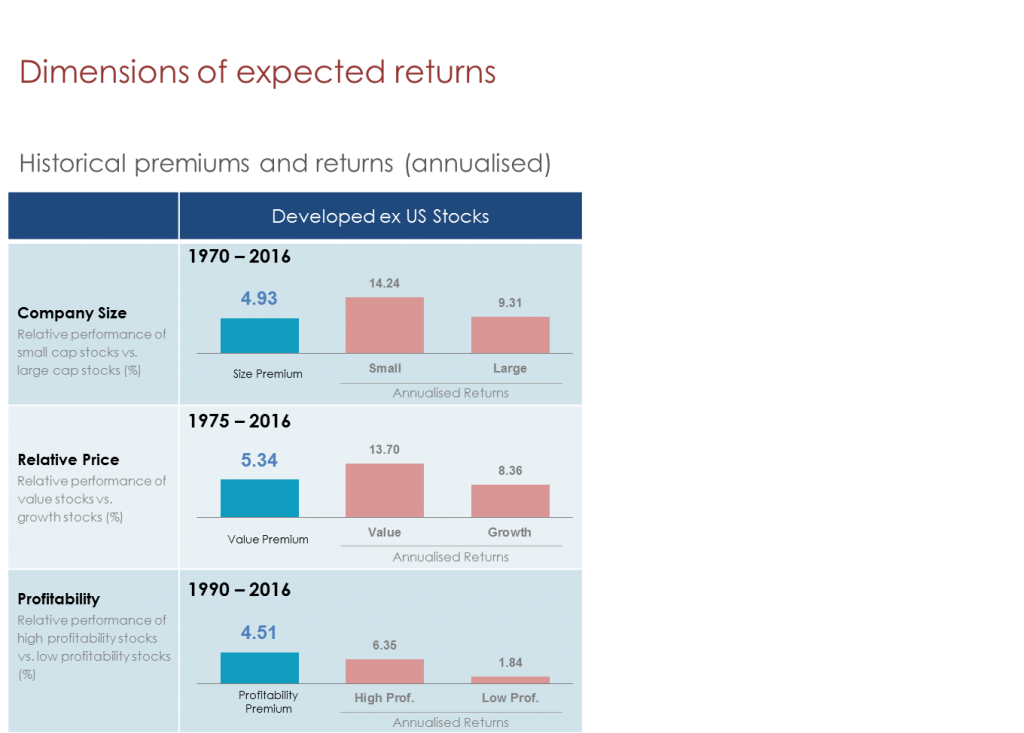

Company Size

Smaller companies tend to deliver a superior return over larger companies over the long term. This is because Risk and Return are related. However it is important to understand they don’t consistently deliver this premium, but if you take a long term approach, tilting your portfolio to this sector will reward the patient investor.

Relative Book-to-Market Value

Often called a ‘Value’ stock, this is where a company’s market value (ie number of shares multiplied by the share price) is lower than its book value (ie the value the accountants give the company). Value stocks have tended to outperform Growth stocks over time, though not all the time. However in the competitive ‘listed company’ world, relative underperformance to peers is not generally tolerated for long. Either the management’s strategy changes or the management changes! This tends to lead to a ‘re-rating’ of such ‘Value’ stocks, and the price generally goes up.

Profitable companies

It may sound obvious but a more profitable company tends to deliver superior returns when compared to a less profitable company in share price terms.

How have these sectors performed relative over time?

Australian Shares

U.S. Stocks

Developed World – Ex U.S Stocks

Emerging Markets

As you can see from the tables above, these premia are observable across all markets over long periods of time. By ‘tilting’ a portfolio to these sectors you increase the probability that over time you will obtain a superior return to the market generally.

Australian Private Capital has implemented this philosophy over many years, obtaining for our clients returns that are superior to the market. Our portfolios are low cost and low trading which enhances after tax returns.

If you have any further questions about APC’s investment philosophy feel free to make contact with a member of our advisory team.

Melbourne Business School – Dean’s Leaders Forum

Australian Private Capital is proud to announce our principal partnership of the Dean’s Leaders Forum for 2017. APC has had a long association with the Melbourne Business School spanning three decades. Along our journey we have sponsored the APC Leadership Breakfast series, the Personal Wealth Management series, presented to alumni on investment principles and have been corporate sponsors of the annual Women and Management dinner.

Our past and continuing involvement with the MBS is based on our strong belief that society as a whole greatly benefits from having well run, innovative business enterprises. This does not happen by chance but requires insightful, dedicated and inspirational leadership. The work that the MBS undertakes in assisting professionals to become future leaders cannot be underestimated in its importance both to the individuals themselves but also to society generally.

Melbourne Business School Dean Professor Zeger Degraeve says the Forum series, now in its fourth year, has been popular for the School’s diverse student and alumni community.

“Melbourne Business School has been progressing and developing individuals, organisations and knowledge for more than 60 years. Underpinning our mission to be global leaders through the creation, application and dissemination of business and economics knowledge are our strong ties to the Australian and international business community.

Over the past three decades, Australian Private Capital has contributed to the success of Melbourne Business School, by supporting our School to deliver a world class business education experience. I am delighted that this relationship will enter a new chapter in 2017, with Australian Private Capital joining us as the Principal Partner for the Dean’s Leaders Forum series.”

MBS Director of Corporate Relations – Alex Christou, MBS Dean – Zeger Degraeve, and Australian Private Capital Directors Robert Sarafov and Hayden Windsor

Australian Private Capital is very much looking forward to hearing from members of Australia’s business leadership elite, as they share their stories, experience and wisdom. The entire APC team is excited to be a part of this important series.

Welcome Calypso and Hiro to the APC Team

With the promotion of both Simon Ereaut (Practice Manager) and Luke Price (Para Planning Team Leader) there came a need to fill their previous roles. After an extensive search APC is very pleased to announce the appointment of both Calypso Waddell and Hiro Matsumura to the Para Planning Team under Luke’s guidance.

Calypso comes to APC from a small financial planning company where she worked as a Para Planner. She wished to move to an advice firm which operates with a high degree of integrity and personal client service. I’m sure you will agree Calypso has made the right choice!

Hiro also gained industry experience as a Para Planner with a small financial planning company and in his spare time has tutored in Japanese.

Whilst both Calypso and Hiro have adapted seamlessly to the ‘APC Way’ they both bring their own personalities to their roles and add to the enjoyable APC work place.

We welcome them both to our team and would encourage you to do the same when next you are in our offices.